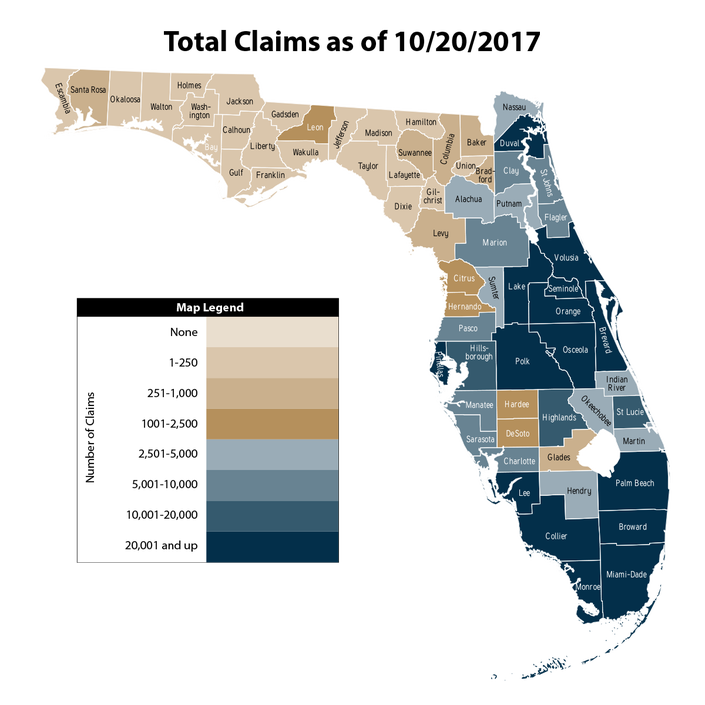

As reported by the Florida Office of Insurance Regulation more than 646,000 residential property claims and over 41,000 commercial property claims were filed as of October 20, 2017. If we include private flood, business interruption and other lines of business claims filed, it is just over 772,900 claims filed and an astounding $5,311,772,141.00 in estimated insured losses!

Brevard County had 35,531 of the 772,900 claims in Florida and more than a month after Hurricane Irma reared her ugly winds and rain our way there are 21,847 claims still open. We at Natwick Insurance are grateful to have had our business and homes spared so we could be there to help our clients immediately after Hurricane Irma passed. Living in our beautiful community we sometimes forget why having the right protection in place to reduce our risks during hardships like this is so important. There are a number of residents and business owners who had gaps in their coverage that left them without the protection they needed. You would be surprised at how many home and business owners don’t have the right insurance protection in place. On average 3 out of 5 of the clients we serve had gaps in their coverage before working with us that we were able to find and fix. Not only were we able to identify and correct these risks, often times we did it at about the same price! As you can see by the map nearly all of Florida was affected by this Hurricane Season. We found the data from the latest Florida Office of Insurance Regulation interesting and hope you did too. As an independent insurance agency we look forward to having the opportunity to be your advocate to get you the best coverage at the best price to deliver the best results. Article Data Reference: Florida Office of Insurance Regulation reported 10/20/2017 *This aggregate information is compiled from claims data filed by insurers. It has not been audited or independently verified and covers all claims based on filings received by the Florida Office of Insurance Regulation as of October 20, 2017 at 3:00pm. Leading up to September 20, 2017 the Office reached out to insurers that had asserted trade secret protection on their Hurricane Irma claims data to request they waive that assertion so the Office could publish aggregate county level data to the public. Because the Office obtained enough waivers, they were able to report their efforts allowed the release of aggregate Hurricane Irma claims date on a county basis.

0 Comments

Out of state contractors are coming to Florida to assist with Hurricane Irma recovery efforts. While many will appreciate this help, many property owners will be putting themselves at great financial risk given many out of state contractors will not have proper workers' compensation coverage and may not be familiar with the stringent FL building codes. We highly recommend waiting for a properly insured FL based contractor who will be familiar with FL building codes and pull the proper permits. We have included work-comp coverage requirements and helpful information from the Florida Division of Workers' Compensation that you will want to be familiar with when hiring a contractor. Also after the 2004 hurricane season many homeowners who used an out of state roofing contractor ended up having roofs installed with no permits. If a contractor replaces your roof and does not complete the permit process you will ultimately receive no premium credit for having a new roof installed on your home. Just be very careful when hiring a contractor and we are here to help with any of your concerns.

1. Hurricane deductibles: Most homeowners’ insurance policies contain specific provisions related to damage caused by hurricanes, and a key feature is often higher deductibles for losses resulting from a hurricane. Under this provision, homeowners are responsible for paying a percentage of the insured value of the home, generally ranging from 2-10 percent. So for a home insured for $100,000 with a 2-percent hurricane deductible, the policyholder would be responsible to pay out of pocket for the first $2,000 in damages.

2. Wind-driven rain: Damage caused by wind-driven rain – for example, rain blown through poorly sealed door/window openings—is not covered in most instances. While damage caused by wind itself is likely covered (subject to the hurricane deductible), water damage caused by rain seeping into the home through doors/windows generally is not. 3. Repair scams: Homeowners should resist the temptation to sign up with the first repair crew that shows up at their door, and especially should not sign paperwork that assigns the rights and benefits of their insurance policy to someone else. Assignment of benefits scams are a leading cause of rising insurance rates, and fraud artists see a hurricane aftermath as a golden opportunity to prey on unsuspecting homeowners. Insurance policyholders should always call their agent or their insurance company first, to report a loss and determine the best way to proceed. 4. Flood damage: Damage caused by flooding, common in a hurricane, is not covered by standard homeowners insurance policies. A separate flood insurance policy is required for this type of loss. 5. Mitigate and document: Homeowners are expected to mitigate damage to their home to the extent they safely can, and to document their damage. So, putting a tarp over a damaged roof or boarding up a broken window can prevent further losses. Homeowners should document damage by taking photographs and save receipts for any out-of-pocket costs. Praying for our community, friends, and loved ones as we prepare for the arrival of Hurricane Irma. Our office is shuttered and Lord willing we will open quickly after the storm to help with your insurance needs. In the event you need to file a claim please visit our website for Hurricane Irma claims reporting contact information.  Demotech recently downgraded Sawgrass Mutual Insurance Company. If you have a policy with them you will want to be aware of this developing situation. The Natwick Insurance team is ready to help anyone in our community looking for guidance or quote from another insurance company.

Distracted driving trends continue to impact insurance rates! Do you have enough coverage to protect you and your family in the event you are injured by a distracted driver or happen to cause an accident while being distracted? Pay attention out there on the road and another reminder to review your automobile insurance policy and coverage with a Trusted Choice Independent Insurance Agent.

Most Florida homeowner’s insurance companies are Demotech rated and not rated by A.M Best. For many years, most A.M. Best rated companies are no longer offering coverage in FL and if they do are simply not competitive. Demotech recently indicated they would be announcing downgrades for several insurance companies but they just announced they are holding off for now. Natwick Insurance is actively monitoring this situation and you can learn more by reading this article provided by Insurance Journal and written by Amy O'Connor, associate editor or MyNewMarkets.com

|

Contact Us

(321) 735-0381 Archives

November 2019

Categories |

||

RSS Feed

RSS Feed

Navigation |

Social MediaShare This |

Contact UsNatwick Insurance, Inc.

1301 South Patrick Drive Suite 73 Satellite Beach, FL 32937 (321) 735-0381 Click Here to Email Us |

Location |

Natwick Insurance, Inc. - Established 2006